Emily Rowan is Clean Prosperity’s Manager of Federal Government Relations.

After months of negotiations Alberta and Ottawa have agreed on a path forward for industrial carbon pricing. The May 15 implementation agreement — following on the memorandum of understanding signed in November 2025 — is more than just a deal between two governments. It’s the start of rewriting the federal carbon pricing benchmark.

What is the benchmark?

The federal carbon pricing benchmark is the minimum standard every province and territory must meet to run its own industrial carbon pricing system. It aims to put all carbon pricing systems across the country on a level playing field. Miss the bar, and Ottawa steps in with its own backstop system.

The benchmark outlines basic criteria including the headline price trajectory, scope of coverage, and minimum stringency. It gives Canada’s patchwork of provincial systems some national coherence.

In late 2025, Environment and Climate Change Canada (ECCC) released a discussion paper to launch a national consultation on revising the federal benchmark. The federal-Alberta agreement on carbon pricing answers many of the questions in the ECCC paper, but not all of them. Notably absent from the agreement is any mention of minimum coverage requirements, suggesting that the federal government may maintain the status quo.

What the Alberta deal locks into the benchmark

The federal-Alberta agreement sets out a carbon pricing framework for Alberta’s Technology Innovation and Emissions Reductions (TIER) system through 2040. Because Ottawa has to set the same minimum standards for the entire country, the federal benchmark will need to reflect the agreement with Alberta.

Significant parts of the Alberta deal will become the new floor for every provincial industrial pricing system. These include:

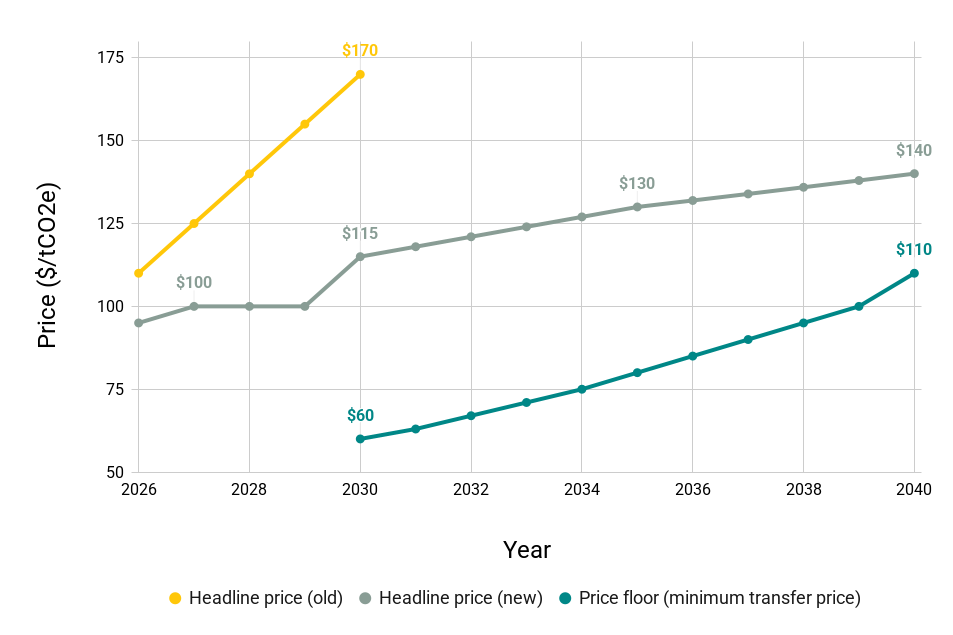

Headline price trajectory: The federal headline price will hold at $95/tonne this year, rise to $100 in 2027, climb incrementally to $130 by 2035, and then increase by 1.5% per year to reach $140 by 2040 The government has formally signaled this change to other provinces.

That’s a significant step down from the previous plan to hit $170/tonne by 2030. Other provinces will now have to decide if they want to maintain the old trajectory or adopt the new minimum benchmark.

Federal headline carbon price trajectory (2026-2040)

The floor price: In Alberta’s TIER system, most emitters can buy credits below the $95 headline price. Credits were trading in the $30-$40/tonne range in early 2026, and well below that for much of the past year. The federal-Alberta deal commits to a price floor of $60/tonne in 2030, rising to $110 by 2040.

The federal government will likely make the price floor a requirement for other provinces through the benchmark. How exactly the floor will operate in Alberta is an open question, but the province has promised to table legislation by the end of the year. Because the federal government lets provinces design their own approaches to meeting the benchmark, each may have to tackle the question for themselves.

We urge provinces to converge in their approaches. This will reduce the complexity for industry and set the stage for future market harmonization.

Benchmark tightening rates: The inclusion of sector-specific tightening rates in the agreement was a surprise to some. ECCC warned that performance benchmarks aren’t tightening fast enough, credit supply is outpacing demand, and the price signal is getting lost. The clear implication was that the benchmark would be updated to address tightening rates and encourage greater abatement across sectors.

Instead, the federal-Alberta carbon pricing agreement set out reduced annual tightening rates across many TIER sectors, including electricity, hydrogen, and oil sands, among others. Some tightening rates will relax further in 2031. At some point these provisions will have to be reconciled with the federal benchmark and the requirement that credit supply not exceed demand.

Direct investment compliance option: The federal-Alberta agreement formalizes federal acceptance of Alberta’s direct investment compliance pathway. This will allow projects to apply for up to half their capital and operating costs to generate compliance credits.

ECCC’s discussion paper expressed concern that this type of approach, dubbed Emissions Reductions Accounts (ERAs), could threaten both the marginal price signal and credit demand. They invited feedback on whether these pathways could be designed to preserve market integrity.

This inclusion in the federal-Alberta agreement sets something of a precedent. The obvious question is whether other provinces will follow suit. The question is different in Ontario, as the only other province with a direct investment-style pathway at the moment, the Emissions Performance Program (EPP). There the question is what changes might still be necessary to bring the EPP into alignment with a revised benchmark.

What probably won’t be in the benchmark

Carbon contracts for difference: Carbon contracts for difference (CCfDs) are probably the most important element of the Alberta deal that won’t feature in the revised benchmark. CCfDs probably don’t fit in the benchmark because they don’t directly relate to the federal government’s mandate to establish “minimum national standards of GHG price stringency to reduce GHG emissions.”

Ottawa and Alberta agreed to jointly issue CCfDs covering up to 75 million tonnes of emissions between 2030 and 2040. These are government-backed guarantees that protect low-carbon projects against the risk of future carbon price changes.

While the federal government hasn’t yet extended this offer to other provinces, doing so would make a lot of sense. CCfDs offered jointly by the federal and provincial governments align with Ottawa’s interest in strengthening the industrial pricing system and providing greater certainty to investors.

If and when the federal government will choose to expand the CCfD program remains to be seen. Ideally Ottawa and Alberta would first sort out the details of the program they’ve agreed on. However the natural window of opportunity for broadening the CCfD program to other provinces, namely the benchmark review and the 2026 federal budget, might be upon us before all the details of the Alberta deal are hammered out.

Next six months are critical

The federal government is still considering input from provinces and industry on the final benchmark design. That makes the coming months consequential.

Credit oversupply is already distorting price signals in several provinces. The benchmark needs to require net demand at a level above the price floor to incentivize emissions reductions. The floor price should be the fallback when things don’t work out as planned.

With many jurisdictions likely to re-open their systems, the federal benchmark update is also a valuable opportunity to harmonize systems and create the conditions for linking carbon markets.

The hard design work is just beginning. The fully updated benchmark is likely to land later in 2026, which means decisions on net demand, credit market structure, and provincial flexibility are being made in real time. Alberta and Ottawa are still working out the details of their joint CCfD program, which could have implications for other provinces.

For anyone with a stake in Canada’s industrial carbon markets, the next six months could matter as much as the Alberta carbon pricing deal itself.